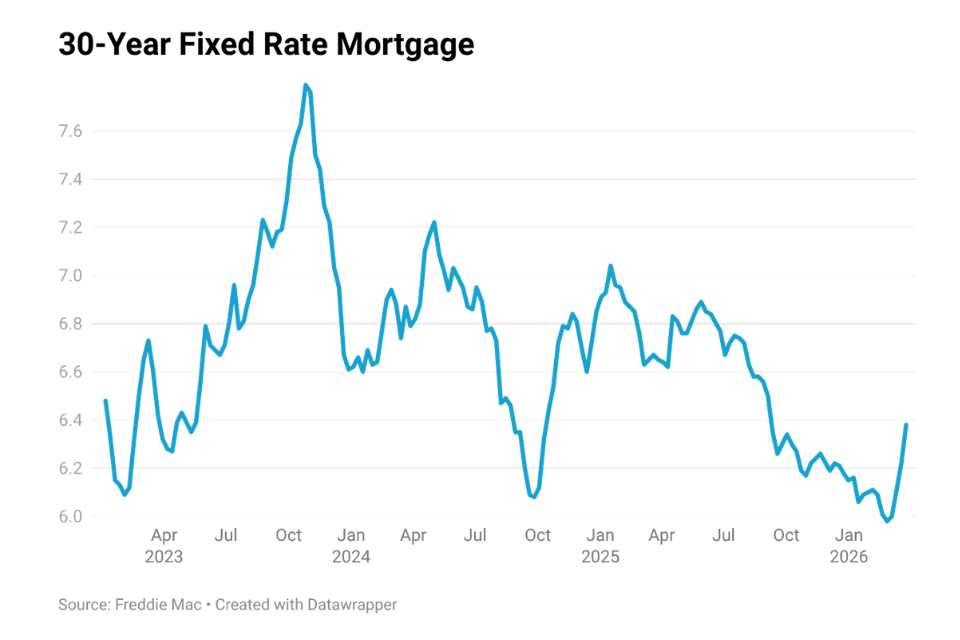

The average 30-year fixed mortgage rate climbed from 5.98% at the end of February 2026 to 6.38% just four weeks later, marking a sharp increase in borrowing costs. Late February had brought a sense of cautious optimism, as declining rates began to stir a spring housing market in need of momentum. That momentum proved short-lived. By mid-March, rising oil prices tied to the war in Iran, along with higher Treasury yields, had pushed rates upward and replaced optimism with renewed concern.

The conflict in the Middle East has driven oil prices above $110 per barrel and contributed to volatility in bond markets throughout March. With no clear resolution in sight, the risk remains that energy prices and the market instability they bring could move even higher. Financial markets have since recalibrated expectations for monetary policy. Investors are now assigning little to no probability of a Federal Reserve rate cut this year, a notable shift from earlier forecasts.

The impact on U.S. consumers is already visible. Average gasoline prices rose above $4 per gallon on March 31, 2026, the highest level since the summer of 2022. But the effect extends well beyond the pump. Higher oil prices increase the cost of transporting goods and raise input costs across agriculture, materials and packaging, pushing prices higher throughout the economy. Even if the conflict were to end immediately, supply disruptions are likely to persist given the extent of damage to energy infrastructure, which will take time to repair. Forecasts are already adjusting. A Reuters survey conducted in March projects Brent crude will average $82.85 per barrel in 2026, roughly 30% higher than the $63.85 estimate published in February before the conflict began.

As expectations for inflation rise, investors demand higher returns on long-term assets, pushing up bond yields, and, in turn, mortgage rates. The 10-year Treasury yield has been moving higher as markets re-price these risks. Even relatively small increases in rates can have an outsized impact. A move from 6.0% to 6.5% materially changes monthly payments, particularly in a market where affordability is already stretched. Many buyers are operating within tight financial constraints, making them highly sensitive to shifts in borrowing costs. When rates rise quickly, demand tends to pull back just as fast.

For sellers, the environment is equally complex. Elevated rates continue to lock in existing homeowners who secured mortgages at much lower levels in prior years. This “lock-in effect” constrains inventory, limiting the number of homes available for sale. While that supply shortage can support home prices, it also reduces transaction volume, keeping overall market activity subdued. Refinancing activity remains muted for the same reason. With current mortgage rates well above the levels many homeowners already hold, there is little financial incentive to refinance.

The broader implication is that housing is being squeezed from multiple directions. Rising rates are reducing demand, while elevated costs, driven in part by energy prices, are preventing a meaningful reset in supply. Even if home prices stabilize or soften in some markets, higher financing costs can offset those gains, leaving affordability largely unchanged. Until inflation pressures ease and bond yields stabilize, mortgage rates are likely to remain elevated and housing activity will continue to reflect that constraint.