For much of early 2026, inflation appeared to be stabilizing. Price increases had moderated from prior highs, and there was growing confidence that inflation might continue to ease through the year. The March data disrupted that narrative.

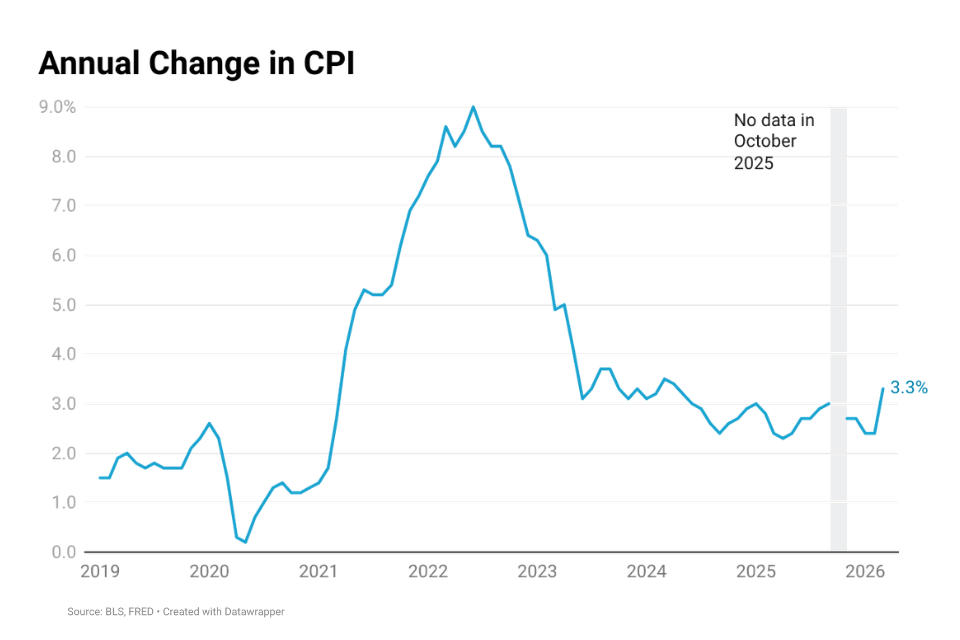

The latest Consumer Price Index report for March 2026 from the Bureau of Labor Statistics showed that inflation rose 0.9% compared to the previous month (the highest monthly gain since June 2022) and 3.3% over the past year, a two-year high. That is a significant acceleration, particularly compared to the more modest increases seen in prior months.

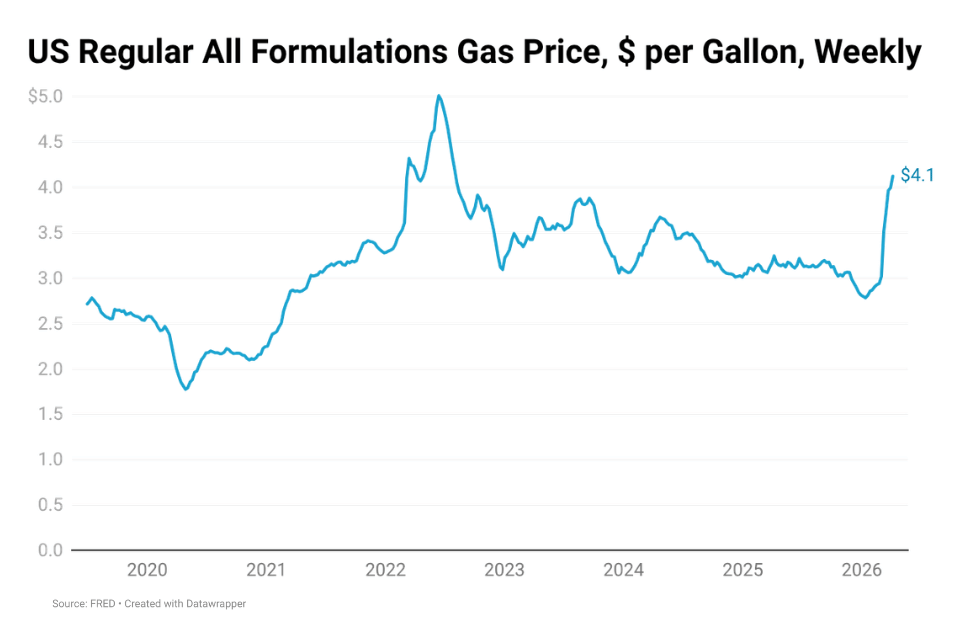

Energy prices surged in March by 12.5% on an annual basis, with gasoline rising 18.9% y-o-y, and fuel oil increasing 44.2% y-o-y. At the same time, core inflation, which excludes food and energy, remained comparatively moderate at 2.6% year over year. Oil prices have risen in response to the ongoing conflict involving Iran, which has disrupted global energy markets. When supply uncertainty increases in oil markets, prices tend to adjust quickly. That adjustment flows directly into gasoline prices and, by extension, into the inflation data.

What makes this dynamic more challenging is that energy prices are not easily or quickly reversed. Oil markets respond to global supply conditions, and when those conditions are disrupted, the adjustment process can take time. Infrastructure constraints, supply chain disruptions, and continued uncertainty can all keep prices elevated even if demand does not materially increase. As of April 10, 2026, activity through the Strait of Hormuz remained limited despite a two-week ceasefire, reflecting continued supply concerns. Traders have begun pricing in a more sustained disruption, which is keeping oil prices elevated.

The United States is the largest oil producer in the world, with daily crude production of about 13.26 million barrels, yet it is not shielded from supply disruptions in the Middle East. The U.S. does not produce all the oil it consumes and continues to import roughly 6.5 million barrels of crude per day, with only a small share coming from the Middle East, while also exporting both crude and refined products. At first glance, this might suggest that events in the Middle East should have limited impact on U.S. energy prices. In reality, oil is traded in a global market where prices are determined by worldwide supply and demand. Oil flows to the highest bidder, and oil producers, whether in the U.S. or elsewhere will sell based on market prices. As a result, disruptions anywhere in the global supply chain push prices higher everywhere, including in the United States.

The impact does not stop at the pump. Higher oil prices feed into transportation costs, logistics, agricultural goods, and production expenses across the economy. Goods become more expensive to move, inputs become more costly, and those increases begin to show up in broader pricing. This is why energy-driven inflation tends to spread, even if it originates in a single sector.

This spike in inflation is an unwelcome development for homebuyers who had hoped 2026 would bring some relief on affordability. Rising costs are already putting pressure on household budgets, reducing purchasing power. At the same time, higher inflation is likely to keep borrowing costs elevated, further tightening affordability. If these pressures persist, they could begin to show up in housing activity through fewer mortgage applications, a slowdown in listings and sales, and an increase in contract cancellations.

The March CPI report reflects the early stages of that process. It captures the immediate impact of rising energy costs, but it does not suggest that those pressures will dissipate quickly. Even if conditions stabilize, the lag between supply disruptions and price normalization can be significant. When inflation is driven by energy, it can persist even when other components of inflation remain contained.