There’s a growing risk in the housing market that isn’t showing up in headlines: insurance.

While mortgage rates, inflation, and inventory dominate the conversation, the cost and availability of homeowners insurance is quietly becoming a consequential force in housing. And unlike interest rates, this is not a cyclical issue.

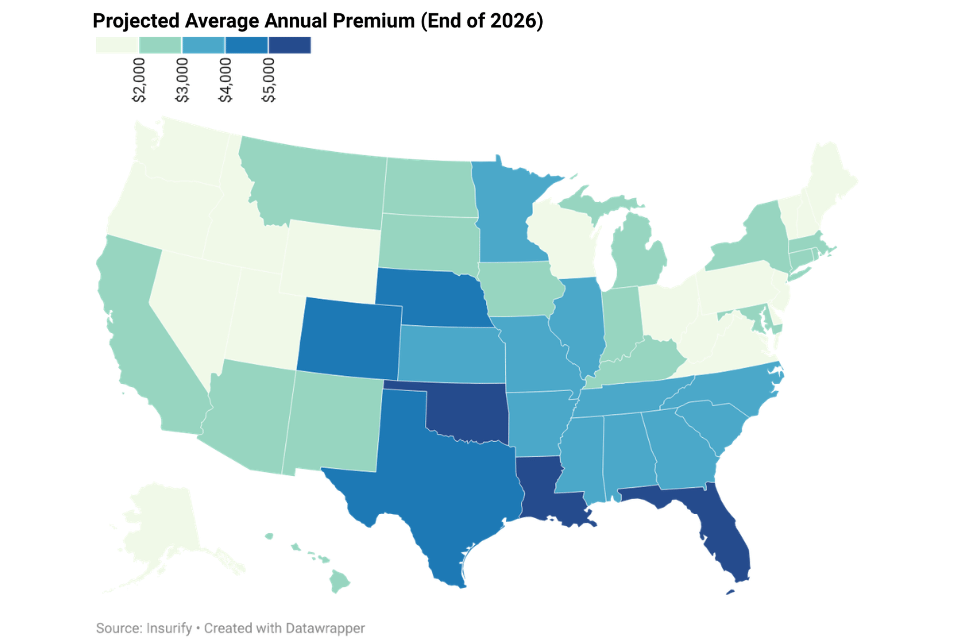

According to Insurify, the average annual cost of homeowners insurance in the U.S. is expected to reach $3,057 by the end of 2026, following a 12% increase in 2025. Rates rose more than 20% in six state – Minnesota (34%), Colorado (33%), Iowa (28%), Nebraska (25%), Oklahoma (24%) and South Carolina (20%). Since 2021, the average cost has risen by more than $900—an increase of roughly 46%. Insurify also forecasts that premiums in states such as California, Nebraska, New Mexico, and Georgia will climb by 10% or more by year-end.

Across large parts of the country, particularly in climate-exposed regions like Florida, California, and parts of the Gulf Coast, insurance premiums have risen sharply. Midwest and Great Plains states have recently experienced stronger increases, driven by their exposure to severe convective storms, including hail, heavy rainfall, high winds, and tornadoes. In 2025, these storms surpassed hurricanes as the leading source of global insurance losses since 2000. In some cases, coverage has become difficult to obtain altogether. Major insurers have pulled back from high-risk markets, leaving homeowners to rely on last-resort state-backed plans that are often more expensive and less comprehensive. While natural disasters are destroying homes, inflation is making them more expensive to rebuild. Home insurance premiums are largely tied to reconstruction costs, and the price of building materials has risen by 15% over the past year.

This shift is not theoretical. It is already changing the math of homeownership.

For buyers, insurance is no longer a secondary expense, it has become a central affordability constraint. A home that looks manageable based on price and mortgage rate can quickly fall out of reach once insurance costs are included. In higher-risk areas, premiums can add hundreds, and in some cases thousands, of dollars annually to the cost of ownership. Unlike mortgage rates, these costs cannot be reduced through refinancing. As a result, some households are opting to go without insurance, leaving their assets exposed to significant risk. In 2023, only 88% of homeowners carried any form of homeowners insurance, with roughly half of the uninsured earning less than $40,000 annually.

The financial strain is already showing up in consumer behavior. A survey by Insurify found that 57% of policyholders have made financial trade-offs to afford coverage, cutting back on nonessential spending (30%), delaying home repairs (22%), and even taking on debt (15%). Additionally, 40% report spending more on home insurance than on other types of coverage, such as auto or health insurance. Under this pressure, more than one in four homeowners (28%) say they would drop their home insurance if it were an option.

For lenders, the implications are equally significant. Insurance is a prerequisite for most mortgages. If coverage becomes too expensive or unavailable, transactions simply don’t happen.

In markets where insurance costs are rising fastest, early signs of stress are already visible. Demand is softening. Time on market is increasing. Sellers are facing greater competition, not just from other listings, but from the total cost of ownership that buyers must now absorb.

This dynamic is particularly acute in parts of the Sun Belt that saw rapid price appreciation during the pandemic. Many of these markets are now contending with a combination of elevated home prices, rising insurance premiums, and increasing supply. The convergence of these factors is beginning to weigh on demand.

The insurance issue also introduces a new layer of inequality into housing. Wealthier buyers may be able to absorb higher premiums or self-insure to some extent. For first-time buyers and middle-income households, those costs can be prohibitive. Over time, this could further segment the housing market, reinforcing existing divides.

Perhaps the most important and least discussed aspect of this trend is that it is unlikely to reverse quickly. Insurance pricing is being driven by underlying risk: climate exposure, frequency of natural disasters, and the cost of rebuilding. These are long-term factors, not short-term fluctuations.

Even if mortgage rates decline, insurance costs could continue to rise. And yet, this risk remains largely underappreciated in market narratives.