Institutional investors have become one of the most debated topics in housing. Many prospective homebuyers believe Wall Street firms continue to dominate the single-family housing market, making it more difficult for families to purchase homes. While institutional investors have undoubtedly influenced certain markets, today’s investor landscape looks different than it did during the pandemic housing boom.

Recent data suggest that investor activity remains an important part of the housing market, but the composition of that activity has changed significantly. Large institutional investors have scaled back acquisitions, while smaller investors continue to purchase homes at a steady pace. At the same time, Congress recently enacted one of the most significant federal housing laws in decades, aimed in part at limiting large-scale institutional ownership of single-family homes while encouraging new housing construction.

Investor Activity Has Stabilized Despite a Slower Housing Market

Housing investors have remained active despite elevated mortgage rates and historically low home sales. According to Realtor.com, investors purchased approximately 534,000 homes in 2025, representing 11.3% of all home purchases, compared with 11.0% in 2024. Investor purchases increased slightly in 2025 compared to 2024 even as purchases by traditional homebuyers declined, demonstrating that investors continue to view residential real estate as an attractive long-term investment.

However, those headline numbers mask an important shift.

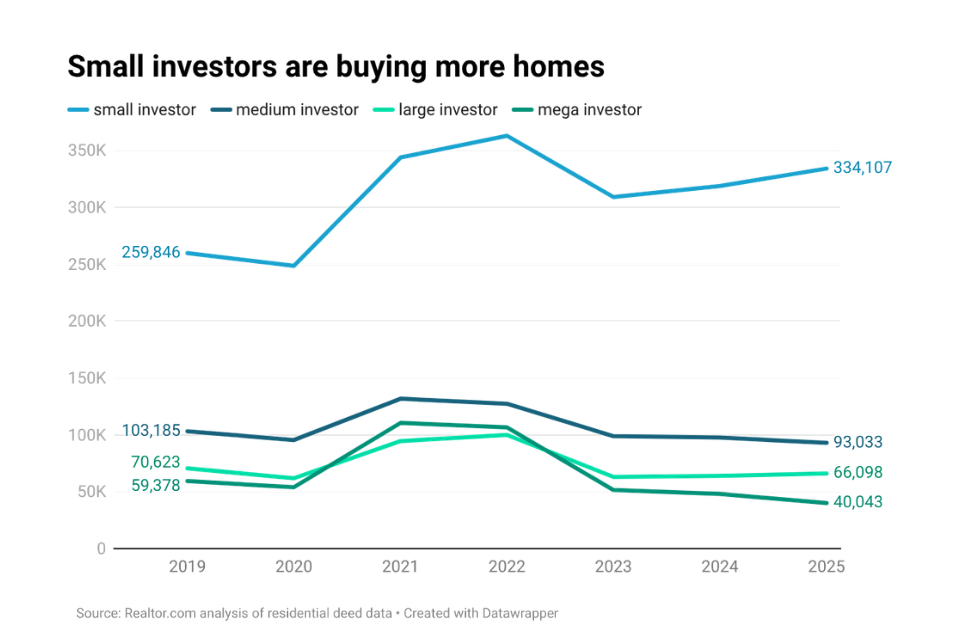

Wall Street Is Retreating While Small Investors Take Its Place

The pandemic years saw substantial activity from institutional investors purchasing single-family homes, particularly across the Sun Belt. Rising home prices, historically low borrowing costs, and strong rental demand created attractive investment opportunities.

Today’s environment is very different.

Realtor.com reports that mega-investors (those have made cumulative all-time purchases of 350 or more homes), have dramatically reduced their acquisitions from over 110,000 in 2021 to 40,000 in 2025. Instead, most investor purchases are now being made by small (1-10 cumulative all-time purchases) and medium-sized (cumulative all-time 11-50 purchases) investors, many of whom own only a handful of rental properties. The share of small investors of all investor purchases climbed from 53% at the pandemic peak to roughly 63% in 2025. Rather than large Wall Street firms dominating the market, local investors and individual landlords now account for majority of investor activity.

This distinction is important because smaller investors often operate in local markets and have different investment objectives than institutional buyers managing thousands of homes. Further, nationwide, small investors typically purchase homes with a median price of approximately $330,000, compared with the overall market median of $440,000. This indicates that they generally are not competing for the typical homebuyer purchase, but instead concentrate on lower-priced properties, including entry-level homes and more affordable housing markets.

Higher Mortgage Rates Have Reduced Investor Demand

Investors face many of the same challenges confronting traditional homebuyers.

Mortgage rates near 6.5%, slower home price appreciation, higher insurance premiums, elevated property taxes, and rising maintenance costs have reduced expected investment returns. As financing costs have increased, fewer properties generate attractive cash flow, causing many investors to become more selective. In 2022, investors purchased nearly 700,000 homes, with that number dropping to 534,000 in 2025.

Investors Continue to Focus on Affordable Markets

Although investor activity has slowed nationally, it remains concentrated in specific regions.

Markets with relatively affordable home prices, strong population growth, and favorable rental economics continue to attract investors. Many Midwestern and Southern metropolitan areas remain attractive because purchase prices are lower than on the coasts while rental demand remains relatively healthy. Investor buyer shares were highest for Memphis (23.7%), Kansas City (21.2%), St. Louis (21.1%), Birmingham (21.0%), Oklahoma City (17.9%). On the flip side, investor buyer shares were lowest in Portland, OR (5.8%), Sacramento (6.1%), Hartford (6.1%), Seattle (6.4%), and Boston (7.0%).

New Federal Housing Law Targets Institutional Investors

The policy landscape has also changed.

In July 2026, Congress enacted the bipartisan 21st Century ROAD to Housing Act, the most significant federal housing legislation in more than three decades. Among its many provisions, the law seeks to reduce the influence of large institutional investors in the single-family housing market while encouraging additional housing construction through regulatory reform, streamlined approvals, and modernization of manufactured housing rules.

The legislation is intended to improve housing affordability over the long term by expanding housing supply and reducing competition from very large institutional buyers. Most economists expect any impact to occur gradually, as housing affordability remains driven primarily by the imbalance between supply and demand rather than investor purchases alone.

Investors Remain Important, but They Are No Longer Driving the Market

Investor activity remains an important component of today’s housing market, but it is no longer the dominant force it was during the pandemic boom. Elevated mortgage rates, slower price appreciation, and higher operating costs have reduced investment activity alongside purchases by traditional homebuyers.

At the same time, the market itself has evolved. The retreat of large institutional investors, the continued presence of smaller local investors, and new federal housing legislation suggest that the investor landscape is becoming more balanced.