Affordability Pinch for Buyers

High mortgage rates combined with elevated home prices mean that monthly mortgage payments for new buyers are substantially higher than just a few years ago. Broader economic concerns, including geopolitical tensions, market volatility, and unpredictable policies, along with continued inflation above the Fed’s target and a cooling labor market, are making both buyers and sellers cautious. These factors have significantly shrunk the pool of qualified buyers, particularly first-time home buyers or those without substantial equity.

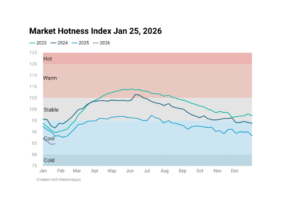

Buyers are being very cautious and only making offers on “the right home,” leading to some homes sitting longer, but not necessarily leading to immediate price drops on desirable properties. Many potential buyers are holding off on major financial decisions, hoping for more clarity on the economic outlook or for rates to come down. Low demand is evident from recent data from the National Association of Realtors showing that the total number of existing sales fell to a seasonally adjusted annual rate of 3.93 million in June 2025, a nine month low. However, sales were unchanged on a year-over-year basis in June. Despite these subdued sales figures, home prices continue to grow, albeit at a slow pace. According to NAR data, the median sale price of an existing home increased from $426,900 in June 2024 to $435,300 in June 2025.

Seller Reluctance and the "Lock-in Effect"

A major factor is that many existing homeowners secured very low mortgage rates (often below 4%) during the pandemic. They are reluctant to sell and buy a new home at today’s much higher rates (hovering around 6.6% or higher), as it would mean a significantly higher monthly payment. This creates a “lock-in effect” where potential sellers are choosing to stay put rather than list their homes, limiting the actual available inventory, even if new listings are appearing. Many would rather wait out the market than lower their asking price.

Still-Low Overall Inventory (Historically)

While inventory levels are gradually increasing and are higher than the extreme lows seen during the pandemic, they are often still below pre-pandemic levels in many areas. This means that despite a slowdown in demand, there isn’t an overwhelming surplus of homes for sale across the board to force widespread price cuts. Supply hasn’t yet caught up enough to significantly outpace demand in most places.

Seller Sentiment and Price Stickiness

Sellers are generally unwilling to lower prices unless absolutely necessary or offer concessions. They might opt to withdraw their listings (delist) and wait for better market conditions rather than accept an offer below their expectations. This “price stickiness” means that home prices move up easily in hot markets but tend to resist downward pressure unless sellers are truly forced to sell due to financial distress or life events.

Regional Variation

The national picture can be misleading. While some previously fast-growing Sunbelt metros are seeing softening conditions, longer times on market, and more price cuts (due to a surge in new construction outpacing local demand and affordability pressures), other markets, particularly in parts of the Northeast and Midwest, remain more competitive with tighter inventory and relatively affordable pricing. These regional strengths can keep the national average from declining sharply.